Some bank services, including expedited payments, bank drafts, and in some cases paper bank statements, may come with additional bank fees. If a company is unaware of the exact amount of these fees, they may not be included in the company’s financial records and will only be seen when they receive their bank statement. Bank charges are service charges and fees deducted for the bank’s processing of the business’s checking account activity. If you’ve earned any interest on your bank account balance, it must be added to the cash account.

Bank Reconciliation Process

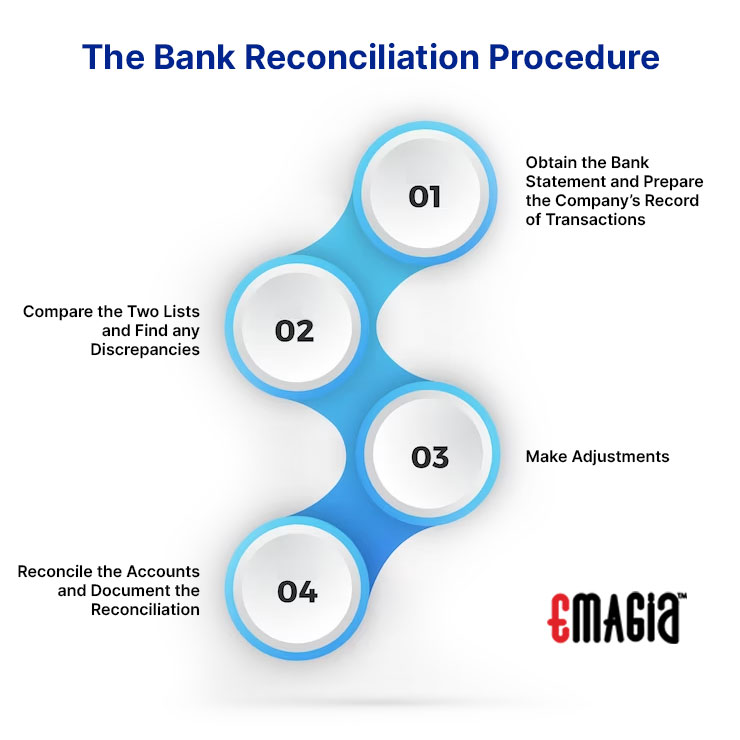

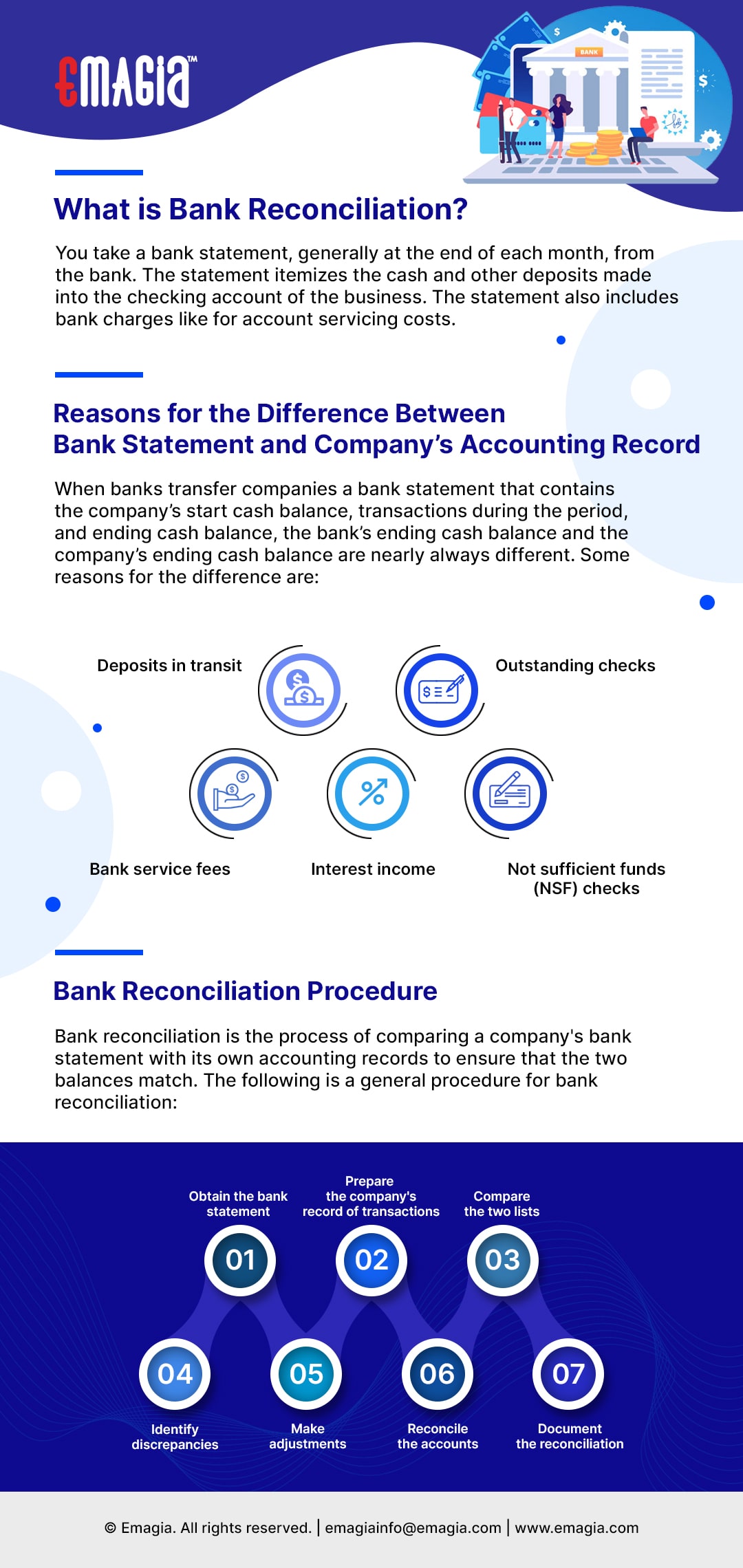

If outstanding checks are left uncompleted, making comparisons to other financial records will be impossible. Add the amount of deposits in transit and subtract the amount of any outstanding checks from your bank statement’s cash balance to arrive at (and record) an adjusted bank balance. Similarly, add any interest payments or bank fees to your business’s cash accounts to find your adjusted cash balance. To reconcile your bank accounts, you’ll first need a copy of your most recent bank statement and access to your business’s accounting records. Specifically, you’ll want access to the general ledger and cash book, which records your cash and bank transactions. Compare each bank transaction to the corresponding transaction as recorded in your general ledger, ensuring the documents match.

Identify Discrepancies

Greg’s January financial statement for the company shows $100,000 in cash, but the bank statement shows only $88,000. Errors in the cash account result in an incorrect amount being entered or an amount being omitted from the records. The correction of the error will increase or decrease the cash account in the books. Deposits in transit are amounts that are received and recorded by the business but are not yet recorded by the bank. When your balance as per the cash book does not match with your balance as per the passbook, there are certain adjustments that you have to make in order to balance the two accounts.

Effect of Time Intervals On Bank Reconciliation Statements

To help you master this topic and earn your certificate, you will also receive lifetime access to our premium bank reconciliation materials. These include our visual tutorial, flashcards, cheat sheet, quick tests, quick test with coaching, and more. This is an important fact because it brings out the status of the bank reconciliation statement. Since these items are generally reported to the company before the bank statement date, they seldom appear on a reconciliation. Once you’ve completed the balance as per the bank, you’ll then need to work out the balance as per the cash book. However, sometimes there are differences between the two balances and so you’ll need to identify the underlying reasons for such differences.

Because the process involves tracing every transaction in their bank account to its original purpose, businesses have the opportunity to see which expenses had the greatest payoffs and which were inefficient uses of their money. The bank reconciliation is an internal document prepared by the company that owns the checking account. After reviewing all deposits and withdrawals, adjusting the cash balance and accounting for interest and fees, your ledger’s ending balance should match the bank statement balance. If the two balances differ, you’ll need to look through everything to find any discrepancies.

What is the purpose of a bank reconciliation statement?

A merchant’s bank account must pay an interchange fee to the card-issuing bank each time someone uses a credit or debit card to purchase something from their store. While both are essential for managing online transactions, there are several differences between payment processors vs. payments gateways. Note that the transactions the company is aware of have already been recorded (journalized) in its records.

QuickBooks then shows you all the transactions you entered into the software during the same time period. You’ll compare the two lists and check a box next to each QuickBooks transaction that also shows up on your bank statement. If you don’t see a balance of zero, QuickBooks helps you troubleshoot the errors and reconcile your accounts.

Michelle Payne has 15 years of experience as a Certified Public Accountant with a strong background in audit, tax, and consulting services. She has more than five years loans and grants of experience working with non-profit organizations in a finance capacity. Keep up with Michelle’s CPA career — and ultramarathoning endeavors — on LinkedIn.

NSF checks are an item to be reconciled when preparing the bank reconciliation statement, because when you deposit a check, often it has already been cleared by the bank. But this is not the case as the bank does not clear an NFS check, and as a result, the cash on hand balance gets reduced. These fees are charged to your account directly, and reduce the reflected bank balance in your bank statement.

When you compare the balance of your cash book with the balance showcased by your bank passbook, there is often a difference. One of the primary reasons this happens is due to the time delay in recording the transactions of either payments or receipts. Likewise, ‘credit balance as per cash book’ is the same as ‘debit balance as per passbook’ means the withdrawals made by a company from a bank account exceed deposits made. For one thing, it helps you catch financial mistakes before they become bigger problems. For example, if you entered a check amount into your general ledger but forgot to physically cash that check, you’ll discover the error during the bank account reconciliation process. To quickly identify and address errors, reconciling bank statements should be done by companies or individuals at least monthly.

- At Business.org, our research is meant to offer general product and service recommendations.

- For example, the payees may be contacted to determine if the checks have been misplaced.

- Once you have identified all the differences between the two statements, identify the source of the discrepancy.

- 11 Financial’s website is limited to the dissemination of general information pertaining to its advisory services, together with access to additional investment-related information, publications, and links.

- A bank reconciliation is a process performed by a company to ensure that its records (check register, general ledger account, balance sheet, etc.) are correct.

Once you have identified all the differences between the two statements, identify the source of the discrepancy. Common sources include deposits in transit that have not yet been deposited in your bank account, as well as bank fees that have been withdrawn by your bank but may have been missed in your company records. A bank reconciliation compares a company’s cash accounting statements against the cash it has in the bank. A bank reconciliation is used to detect any errors, catch discrepancies between the two, and provide an accurate picture of the company’s cash position that accounts for funds in transit. Before you reconcile your bank account, you’ll need to ensure that you’ve recorded all transactions from your business until the date of your bank statement. If you have access to online banking, you can download the bank statements when conducting a bank reconciliation at regular intervals rather than manually entering the information.